Wyoming’s coal industry — a longtime powerhouse of the state economy — faces headwinds that experts say may strengthen with time.

In the last six years Wyoming’s coal production has dropped 16 percent, and coal jobs have dropped 7 percent. The total value of coal produced in 2013 was down $796 million dollars from a peak of $5.9 billion in 2011. Total state revenue from coal mining dropped 8 percent from 2012 to 2013 — a $103 million decline from $1.263 billion to $1.16 billion.

The reasons for the declines include geology and commodity market economics. A recent economic report suggests impending carbon and toxin emissions regulations will be an even bigger hit to an industry that has provided Wyoming’s most stable source of mineral revenue for decades.

Depending on how the Clean Power Plan is implemented Wyoming’s revenue for coal could decrease anywhere from 31.9 percent to 63.1 percent by 2030, according to a study by University of Wyoming economists. That means big potential changes in Wyoming, a state where the value coal mined took 140 years to reach $3.1 billion per year in 2002, and then nearly doubled to $5.9 billion in 2011.

Despite the changing dynamics, State Treasurer Mark Gordon believes it’s too early to say Powder River Basin coal — or Wyoming — is in a bust. “I think we will still sell a pretty substantial volume of coal,” Gordon said in an interview last month. “We are in a period of challenged revenues, but I don’t believe it is a bust. I don’t believe it is anything close to a bust.”

Alpha Natural Resources — owner of the Eagle Butte and Belle Ayr strip mines, the latter the Powder River Basin’s oldest — will be delisted from the New York Stock Exchange. The Wall Street Journal reported last week that the company is in talks to declare bankruptcy.

How the talks play out, and whether other Wyoming coal mining companies will follow or rise from a such a restructuring, will play a major role in Wyoming’s economic future.

“Someone who is a technical expert may say, ‘If we get cheap carbon capture in 50 years, that could turn things around,’ but I don’t think the future outlook for coal is that strong,” said University of Wyoming economist Rob Godby.

Meanwhile, political leaders in Wyoming hope that relief may also come from political change and a more coal-friendly presidential administration beginning in 2017.

Creating an industry

Wyoming’s coal mining industry began in the late 1860s with the construction of the transcontinental railroad. Underground mines along the Union Pacific line across southern Wyoming, and later on the Burlington line in northern Wyoming, helped fuel locomotives, local heating needs, and small power generating stations.

[wpex more=”Click to read more”]

By the 1950s Wyoming had numerous underground coal mines near Sheridan, Rock Springs, and Kemmerer. The industry then collapsed when railroads shifted from coal-fired steam engines to diesel-powered locomotives. By the mid-1960s many coal company-owned mining camps withered or turned into ghost towns, as statewide coal mining jobs dropped from 2,000 in 1954 to just 327 in 1965.

Wyoming’s modern coal industry began in the early 1970s, with rising demand for coal to fuel power plants. Strip-mining techniques opened up shallow deposits in the Powder River Basin, which were less costly to mine than eastern coal.

During the 1980s Wyoming mines dialed up out-of-state exports due to deregulation of rail freight for interstate shipments, and expansion of railroads into the region. Mines invested in enormous haul trucks and drag lines, building economies of scale. During the oil bust of the 1980s the expanding coal industry helped buoy Wyoming’s state revenue and provide jobs.

Then in the 1990s federal regulations to further reduce sulfur dioxide emissions shifted markets to the benefit of Wyoming’s low-sulfur coal. (For more on Wyoming’s coal history, read this university report to the Wyoming Infrastructure Authority.)

[/wpex]

Production

Today Wyoming is by far the largest coal producer in the nation, mining 40 percent of the nation’s supply, and fueling power plants in 34 states. The vast majority of Wyoming’s coal comes from the Powder River Basin, while there are a few relatively small mines in the southwest part of the state.

Wyoming’s coal output peaked in 2008, at 466 million tons, before entering a 15.8 percent decline as of 2014.

Production for 2013 was 388 million tons. More than half of that came from just two mines: 101 million tons from Arch Coal’s Black Thunder mine, and another 110 million from Peabody Energy’s North Antelope Rochelle mine. Together these two mines produced 22 percent of the nation’s coal in 2014, according to the Wyoming State Geological Survey.

Low natural gas prices, rising shipment costs, rail congestion, decreased electricity demand, and concerns about regulation have driven the decrease in production since 2008, according to a University of Wyoming report. Those factors, together with falling prices, reduced the value of Wyoming’s coal production by $796 million since 2011, according to economists.

The decline in Wyoming coal comes amid a slowdown in international coal sales, driven largely by China’s reduced imports and protection of its own domestic mines.

“There is significant oversupply, and demand in China has not been growing fast enough to offset the decline,” Godby said. “China has made it clear they intend to reduce the coal they are using.”

Jobs

Powder River Basin coal mines provide about 6,600 direct jobs in the region, a number that has declined 7 percent from the roughly 7,100 jobs counted in 2010, the UW study found.

Those 6,600 direct coal mining jobs are included the broader coal economy of 17,000 jobs, including transportation, power plant employment and other related jobs in the state. (The total statewide workforce for all industries is about 289,000 jobs.)

The average earnings for a coal miner in Campbell County is $82,654, nearly twice the statewide median of $44,977, according to the study. Overall, one in five Powder River Basin jobs are tied to the coal economy.

Assessed valuation

Assessed valuation — the calculation of property value used for levying state and local taxes — is one useful way to gauge the economic importance of Campbell County’s minerals in Wyoming’s economy. For 2014, Campbell County had a total assessed property valuation of $6.2 billion, the highest in its history. To put that in perspective, the entire state’s 2014 assessed valuation was about $24.1 billion dollars. So about one-quarter of the state’s property tax base is in Campbell County.

Omitting non-mineral property, almost one-third of Wyoming’s assessed valuation for minerals is in Campbell County. In dollar terms, Campbell County minerals had an assessed valuation of $4.6 billion in 2014, while the statewide mineral valuation was $14.4 billion.

The high valuations amid coal’s decline are possible because companies have recently developed significant new oil and natural gas resources in Campbell County. In 2014 Campbell County ranked third in locally assessed oil and gas valuation among counties, exceeded only by Sublette and Sweetwater counties.

However, Campbell County’s coal mines are still worth more than the oil and gas resources in any one county.

Prospects for the biggest players in coal

A large amount of Campbell County’s mineral property is in its two largest mines: Black Thunder, operated by Arch Coal, and North Antelope Rochelle, owned by Peabody Energy. In terms of productivity per worker, these mines are some of the most efficient in the world.

Yet in recent months some observers expressed doubt in the financial strength of these gargantuan mines. One financial analysis in March 2015 predicted that U.S. coal mining companies could face a “wave” of bankruptcies in the near to midterm future.

In particular the report noted that Peabody recently had to pay 10 percent interest in a recent bond offering, unfavorable terms that could pinch other coal companies in need of financing.

“The clouds are darkening over U.S. coal,” concluded writer Nick Cunningham of Oilprice.com.

Economists: Clean Power Plan will slow Wyoming’s coal economy

Coal production in Wyoming is likely to further decrease as the Obama administration implements new carbon rules under the Clean Power Plan — a hit for both Campbell County and Wyoming economies.

Of all the current threats to U.S. coal production, economists say these impending regulations would have the strongest effect on decreasing the production of Powder River Basin mines — with a resulting tumble in Wyoming state revenue. However, market pressures from natural gas and climbing production costs also contribute to mining less coal.

In May of this year the Center for Energy Economics and Public Policy at the University of Wyoming released a report showing the significance of coal in Wyoming’s economy and state revenues, and the potential economic effects of new regulations.

“What the state was hoping for was, ‘We know it is going to be bad, but can we put numbers on how bad it is?’” Godby said.

One of the report’s findings is a projected 32 percent reduction in Wyoming’s coal output by 2030, should proposed regulations come into play. That equates to a production drop of more than 100 million tons from today’s levels.

Under that scenario, the state could lose 7,000 jobs from the 17,000 total in the coal economy, while Campbell County could lose 1 in 10 jobs in all sectors.

Increasing oil and gas production in the county likely wouldn’t make up for the projected number of jobs lost, according to the UW report. However, Godby said some miners may seek work elsewhere, such as in the gas fields near Pinedale and Rock Springs. “You might have employment displacement as opposed to outright loss,” he said.

Projected revenue declines

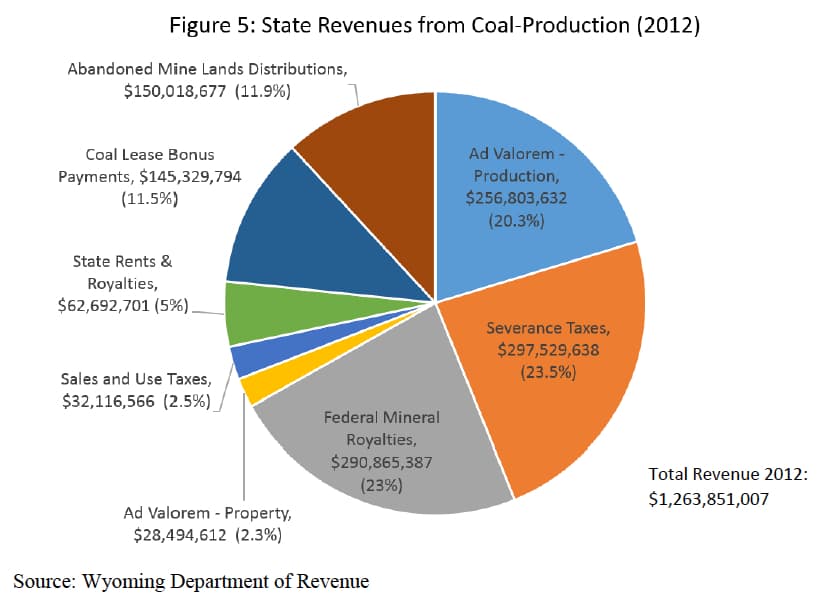

Any hit to coal mining in this energy-rich region could strike a blow to Wyoming’s state revenue. Across all state and local governments, coal mining contributed $1.26 billion in annual revenue in 2012, or 11 percent of the total collected by the state, counties, and municipalities.

Depending on how other states react to the Clean Power Plan regulations, Wyoming could lose 31.9 percent to 63.1 percent of its coal revenue by 2030. Rising natural gas production would dampen that revenue loss somewhat, making for a combined coal and gas revenue decrease of 36 percent to 46 percent by 2030.

Coal revenue in Wyoming comes from a variety of sources, including property taxes, Abandoned Mine Lands Funds, severance taxes, federal mineral royalties, and coal lease bonuses.

School Funding

The toll would be particularly heavy for statewide K-12 education and school construction spending, which rely heavily on Federal Mineral Royalties, property taxes, and coal lease bonuses. Combined, those two divisions of state government spend about $1 billion annually.

“The threat is that is the revenue we use to build schools and support the School Foundation account, in the next decade we could see a major change,” Godby said.

Low prices for oil and gas, plus declining coal sales, have led state budget analysts to project K-12 education will need supplemental funding of $270 million for 2017-2018, and a slightly smaller amount for 2019-2020.

In a June report to the Joint Appropriations Committee legislative staff projected that assessed valuations for property taxes could decrease by 23 percent to 28 percent in the next two years. The decrease in local and state property tax collections, combined with reduced Federal Mineral Royalties, is like a triple-punch to state school revenue.

Since K-12 school spending is guaranteed by law, those funds will have to be made up from other sources such as the Permanent Land Fund Holding Account, which could be drained by 2019 if the scenario pans out, according to the UW report. That, in turn, could require transfers from the General Fund, from investment income, or other sources to make up for the shortfall. The last time Wyoming funded schools from non-education accounts was during a prolonged downturn from 1993 to 2002.

School construction relies primarily on revenue from leasing new tracts of federal land for coal mining. There hasn’t been a successful coal lease sale since June 2012, according to state officials, and no lease sales are expected until the beginning of 2016 at the earliest. If no new sales occur, that revenue stream is projected to go to zero by 2019.

School construction wouldn’t cease as a result, but it would drop significantly by the end of this decade, according to projections. For a much more in-depth look at school revenue projections, see this University of Wyoming report.

Fate in other states’ hands?

Grappling with the prospect of declining revenue, and what if anything the state can do to avert them, is a task for Wyoming policymakers. Yet, much of the problem is out of Wyoming’s hands, according to findings in UW’s coal study. Only a small portion of Wyoming’s coal is consumed in-state.

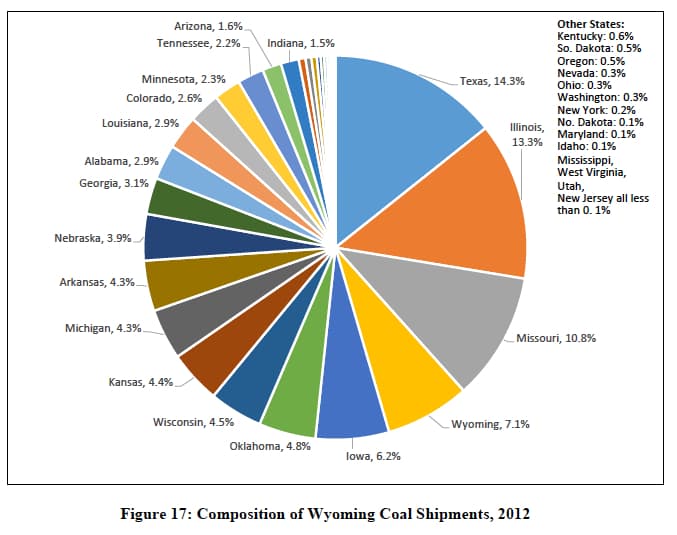

“Wyoming can’t do a lot on its own,” Godby said. “We ship 93 percent of our coal out by rail and another 4 percent out by [transmission] wires. It is not what we are doing with coal, it’s what other people do. Wyoming’s own policies really make no difference.”

That’s why local leaders are focused on fighting federal regulations and putting support behind efforts to enter Wyoming coal into the international export market — particularly the Asia-Pacific market.

Should new coal ports come to fruition in Washington and Oregon, and Wyoming producers secure export contracts, international shipments could balance out production declines to the tune of 100 million tons a year, according to the UW study. That could support up to 4,000 jobs in the Powder River Basin, and contribute $1.2 billion to the state’s gross product, slowing the leak in the revenue bucket.

Even that boost, however, wouldn’t balance out job losses and production declines due to carbon regulations, the study projected. Furthermore, coal companies that have seen their stock prices decline to less than a dollar lack financial strength to complete coal export terminals, especially in the face of local opposition in Washington to potential coal dust and rail congestion, according to the UW report.

Getting other states to play along

If the Clean Power Plan is implemented as written, the best case scenario for Wyoming’s coal production would have individual states using energy efficiency measures to decrease electricity demands, and cooperating with other states to trade carbon reduction credits to meet the quotas in the plan.

That would mean fewer changes on the electrical generation side of the equation, and more potential to continue using coal as a fuel in power plants. What Wyoming policymakers could do to push other states to adopt such policies remains an open question.

“Wyoming hasn’t been trying to influence other states that would be in its own best interest,” Godby said. “They haven’t been banging the drum for more energy efficiency and cooperation.”

“What Wyoming should be doing, by our analysis, is we should be cheerleading any approach that softens the impact on coal,” Godby said of the university report.

A silver lining?

One silver lining to the scenario with the greatest decrease in coal production is that it would also result in the smallest decrease in revenue for the state of Wyoming.

That’s because reduced coal production could bring increases in coal prices, along with more demand for natural gas for baseload electrical generation, Godby said. That would raise prices for both fuels, and create a shallower decline in state revenue.

“It results in this effect that what is worse for the Wyoming [coal] economy is better for Wyoming revenues,” Godby said. “That’s an odd result, but I don’t think we’d be in a situation where lawmakers would say, ‘We need to do what is best for the revenues, not for the state economy,’ because revenues don’t vote, people do.”

Godby says it’s positive that the state is paying attention to the coal situation. “It is good the state is thinking about this, because for a long time the state has taken it for granted that coal is the one resource that has been there the last 35 years,” he said.

Flickr Creative Commons photo by Larry HB.

Clean coal is an oxymoron, heavy on the “moron.” Not much here to give any hope that our grandchildren will not need gas masks in those gold plated school buildings! I don’t see much here about the huge discrepancy between shipping 93% of Wyoming’s coal out to Asia but sending only 4% of it’s coal out of state through electrical transmission lines.

It should be just the opposite.

The onus would then be (perhaps?) on Wyoming’s mega coal burning plants and the massive destruction of it’s own air quality breathed by its own citizens, right here, NOT “out of sight, out of mind” in “communist” China where these citizens have to breathe exhaust from our “Wyoming Clean Coal”…

Bob Cherry